One of the most frustrating moments in dealing with water damage is finding out, after the fact, that your homeowners policy doesn’t cover what happened. Insurance isn’t designed to cover every type of water damage, and understanding the common exclusions before you’re in the middle of a claim can save you a lot of frustration, and in some cases, help you actually prevent an excluded loss in the first place.

Gradual Damage and Long-Term Leaks

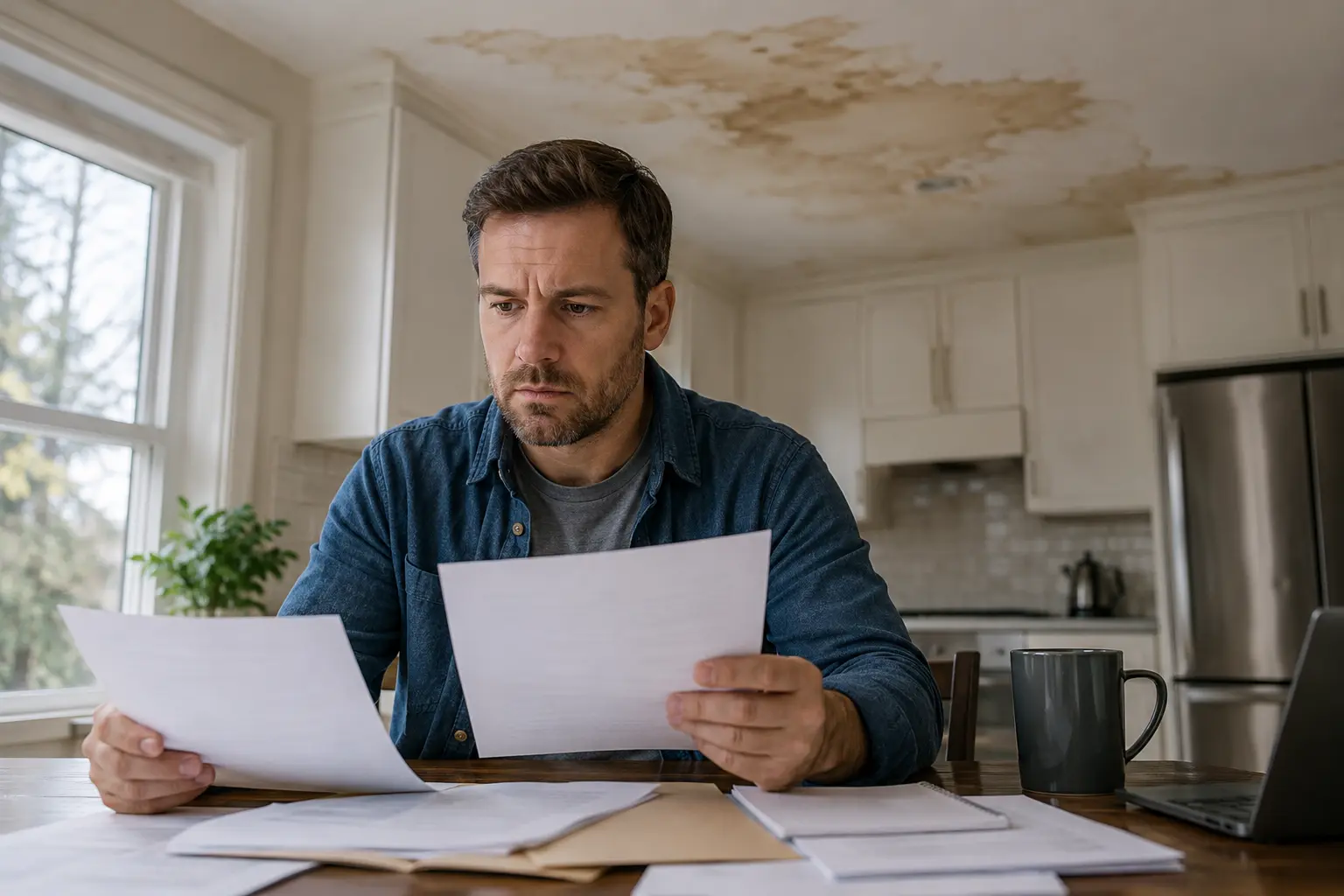

This is the single most common reason water damage claims get denied. Insurance policies are generally designed to cover sudden, accidental events, not damage that developed slowly over time due to lack of maintenance. If an adjuster determines that a leak had been occurring for weeks or months before it was addressed, evidenced by extensive mold growth, rotted wood, or staining that clearly predates a single incident, the claim is often denied as a maintenance issue rather than a covered loss.

This is part of why catching and addressing leaks quickly matters beyond just limiting damage. A slow roof leak that’s allowed to continue for months, even if it eventually causes a dramatic-looking ceiling collapse, is more likely to be classified as gradual damage than if the same leak had been caught and repaired within days. For more on this distinction as it relates to roofs specifically, see our guide on Los Angeles roof leak repair.

Flood Damage From Outside the Home

Standard homeowners insurance policies typically exclude flooding caused by external water sources, like heavy rain overwhelming storm drains, a nearby creek or river overflowing, or general groundwater intrusion. This type of damage generally requires separate flood insurance, usually through the National Flood Insurance Program or a private flood policy, which most homeowners don’t carry unless they’re in a designated flood zone. If your property experienced damage from outside water during a storm rather than from an internal plumbing or appliance failure, it’s worth checking whether you have flood coverage before assuming your standard policy applies.

Sewer and Drain Backups (Without Specific Endorsement)

Many standard policies exclude damage caused by sewer or drain backups unless you’ve purchased a specific sewer backup endorsement, which is often an inexpensive add-on that’s frequently overlooked when policies are first written. Without this endorsement, a sewage backup into your home, even if it wasn’t caused by anything you did, may not be covered at all.

Mold Damage (in Many Cases)

Mold coverage varies significantly between policies and insurers, and many policies cap mold-related coverage at a relatively low dollar amount, or exclude it entirely if the insurer determines the mold resulted from a long-term moisture issue rather than a sudden covered event. This is another reason addressing the root moisture source quickly matters, both for your property and for your insurance position. Our guide on why mold can come back after remediation covers some of the underlying causes that insurers scrutinize when evaluating mold-related claims.

Damage From Lack of Maintenance

If an adjuster can point to a maintenance issue, an old, unmaintained appliance that finally failed, a roof well past its expected lifespan with no documented upkeep, deteriorated plumbing that hadn’t been inspected in years, the claim can be denied on the basis that the homeowner failed to maintain the property in reasonable condition. Keeping basic maintenance records (even simple things like receipts for plumbing inspections or roof repairs) can help counter this argument if a claim is disputed.

Water Damage to Excluded or Unscheduled Items

Even when the underlying water damage claim is approved, certain types of property may have limited coverage or require a specific endorsement, including valuable personal items, certain types of fine art, or business property kept in a home office. It’s worth reviewing your policy’s personal property limits if you store anything particularly valuable in an area at risk for water damage.

Damage That Occurred While the Property Was Vacant

Many policies include a vacancy clause that limits or excludes coverage if a property has been unoccupied for an extended period (commonly 30 to 60 days) when the damage occurred. This matters for vacation properties, properties between tenants, or homes left empty during an extended trip. If you know a property will be vacant for a while, it’s worth checking your policy’s specific vacancy terms and whether a vacant property endorsement is available.

How “Sudden and Accidental” Gets Interpreted in Practice

Most coverage disputes ultimately come down to this exact phrase, and it’s worth understanding how it actually gets applied. “Sudden” generally means the damage happened quickly, over hours or a single day, rather than building up over weeks or months. “Accidental” generally means it wasn’t the result of intentional action or a known, unaddressed problem. A pipe that bursts without warning is both sudden and accidental. A pipe that’s been visibly corroding and slowly dripping for months before it finally gives way is harder to classify as sudden, even though the final failure itself happened quickly, because the underlying deterioration was gradual and, depending on whether it was visible or detectable, arguably something that should have been addressed sooner.

The Role of Photos and Maintenance Records in Disputed Claims

When a claim is borderline between “sudden failure” and “gradual deterioration,” documentation becomes the deciding factor far more often than the actual physical facts of the damage. Homeowners who can produce dated photos showing a property’s condition before the loss, receipts for periodic plumbing or roof inspections, or service records for major appliances are in a meaningfully stronger position than those with no documentation at all. This is worth setting up proactively, not after a claim is already in dispute: a simple folder of dated photos taken every six months to a year of your roof, attic, and any visible plumbing can become valuable evidence if a claim is ever questioned.

Why Some Denials Are Worth Appealing and Some Aren’t

Not every denial is incorrect, and it’s worth being realistic about which situations are worth pursuing further. If the damage clearly developed over an extended period with no reasonable excuse for not catching it sooner, an appeal is unlikely to succeed regardless of how it’s framed. If the denial seems to rest on an assumption not actually supported by the evidence, for example, an adjuster assumes gradual damage based on visible mold, without acknowledging that mold can develop within days under the right conditions following a genuinely sudden event, that’s a much stronger basis for an appeal, particularly with documentation from a restoration company supporting a faster timeline than the adjuster assumed.

What You Can Do If You Can’t Get Sewer Backup Coverage Added

If your insurer doesn’t offer a sewer backup endorsement, or if it’s been declined for a property with a known history of backups, a few alternative steps can reduce your exposure: installing a backwater valve (a plumbing device that prevents sewage from flowing back into your home during a municipal sewer surcharge) is a relatively common solution for older properties in areas prone to this issue, and some cities offer rebate programs to help offset the installation cost.

How Renters Are Affected Differently Than Homeowners

Most of this discussion centers on homeowners insurance, but renters face a parallel set of issues with renters insurance, which generally covers personal belongings rather than the structure itself. If water damage in a rental unit is caused by a building-wide issue, a failing water heater in a shared mechanical room, or a roof leak affecting multiple units, the building owner’s commercial policy typically handles structural repairs, while the renter’s own policy (if they have one) covers their personal belongings, subject to the same general exclusions discussed above for gradual damage, flooding, and similar causes. Renters without renters insurance have no coverage at all for their personal belongings in most water damage scenarios, regardless of who’s at fault, which is part of why renters insurance, often inexpensive relative to the coverage it provides, is worth carrying even in a rental property where the landlord maintains separate building coverage.

How HOA and Condo Master Policies Complicate Coverage

For condo owners, water damage coverage often involves three potentially overlapping policies: the HOA’s master policy (typically covering the building structure and common areas), the unit owner’s individual condo policy (typically covering interior finishes, personal belongings, and sometimes specific building components defined in the HOA’s governing documents), and potentially a neighboring unit’s policy if the damage originated from another unit. Determining which policy applies to which part of the damage often comes down to the specific language in the HOA’s CC&Rs (covenants, conditions, and restrictions) defining what’s considered part of the unit versus part of the common structure. This is an area where disputes are common, and where having clear documentation of the damage’s source and extent matters significantly for sorting out which policy, or policies, ultimately pay for what.

How Multiple Small Claims Can Affect Future Coverage

Beyond whether a single claim gets approved or denied, it’s worth understanding that filing multiple water damage claims over a relatively short period, even small, approved ones, can affect your insurability and future premiums. Insurers track claims history through shared industry databases, and a property with several water-related claims in a few years may face higher premiums, a non-renewal notice, or difficulty obtaining new coverage if you switch insurers. This is part of why it sometimes makes financial sense to pay for a smaller repair out of pocket rather than filing a claim, particularly if the repair cost is only modestly above your deductible, since the long-term premium impact of an additional claim on your record can sometimes outweigh the short-term benefit of the payout.

What an Independent Adjuster Hired by Your Insurer Actually Does

It’s worth distinguishing between three different types of adjusters that can be involved in a claim: a staff adjuster, who is a direct employee of your insurance company, an independent adjuster, who works on a contract basis for insurance companies (often used during high-volume periods like after a major regional storm) but still represents the insurer’s interests rather than yours, and a public adjuster, discussed in detail elsewhere, who is the only one of the three actually working on your behalf. Understanding that both staff and independent adjusters represent the insurance company’s interests, not yours, regardless of how friendly or helpful they seem during the process, is an important and often misunderstood distinction.

What You Can Do If Your Claim Is Denied

- Request the specific policy language the denial is based on, not just a general explanation. Insurers are required to cite the relevant exclusion.

- Get a second, independent assessment of the cause and timeline of the damage, since an independent contractor’s documentation can sometimes contradict an adjuster’s “gradual damage” determination if the actual cause was sudden.

- Review whether the denial reason actually applies to your specific situation, since denials are sometimes issued based on a general policy and not always specific facts of your claim.

- Consider hiring a public adjuster if the claim amount is significant and you believe the denial was incorrect. For more on this option, see our guide on public adjuster vs restoration company.

- File a complaint with the California Department of Insurance if you believe your claim was wrongfully denied and the insurer isn’t responding to your appeal.

How to Reduce Your Risk of an Uncovered Loss

- Address leaks and plumbing issues promptly rather than waiting to see if they get worse

- Keep basic maintenance records for your roof, plumbing, and major appliances

- Consider adding a sewer backup endorsement if your policy doesn’t already include one

- Evaluate whether flood insurance makes sense for your property, even if you’re not in a high-risk flood zone, since a meaningful share of flood claims nationally come from properties outside mapped flood zones

- Document your property’s condition periodically with photos, which can support your position if a “gradual damage” dispute arises later

Understanding these exclusions before you’re in the middle of a claim puts you in a much stronger position, both for preventing avoidable losses and for pushing back effectively if a claim gets denied for a reason that doesn’t actually apply to your situation. For a broader look at how water damage claims work in Los Angeles overall, see our complete guide on water damage insurance claims.

Dealing with water damage and unsure about your coverage? Call ASAP Water Damage Restoration. We help document damage thoroughly and work directly with insurance adjusters throughout the Los Angeles area.