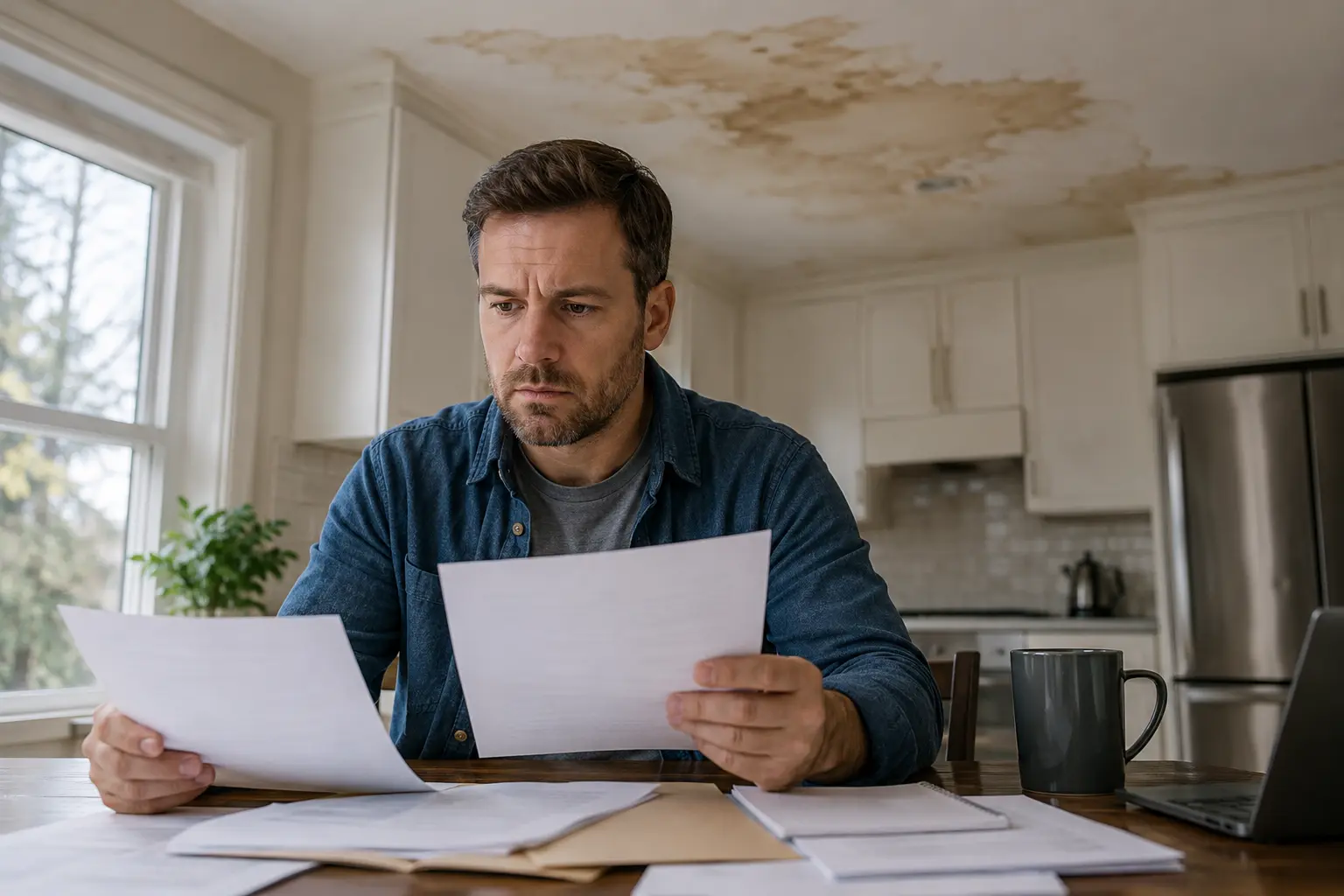

After significant water damage, you’re often dealing with two different kinds of professional help: a restoration company that physically fixes the damage, and potentially a public adjuster who helps you navigate the insurance claim itself. These two roles are often confused, partly because both seem to be “helping with the insurance process” in some way. Here’s how they actually differ and how to figure out if you need one, both, or neither.

What a Restoration Company Does

A restoration company handles the physical recovery of your property: water extraction, structural drying, mold prevention, and rebuilding damaged areas back to their pre-loss condition. Their role is hands-on and technical, focused on actually fixing your home or business. A reputable restoration company will also document damage thoroughly, take moisture readings, and provide detailed invoices, all of which support an insurance claim, but documenting damage for insurance purposes is a byproduct of doing the restoration work properly, not their primary function.

What a Public Adjuster Does

A public adjuster is a licensed professional who represents you, the policyholder, in negotiating with your insurance company. Unlike the adjuster your insurance company sends out (who works for the insurer), a public adjuster works exclusively on your behalf, for a fee that’s typically a percentage of the final settlement amount. Their role includes reviewing your policy to identify all applicable coverage, documenting and valuing your loss (sometimes more thoroughly than an insurance company’s own adjuster), and negotiating directly with the insurance company to maximize your settlement.

When You Likely Don’t Need a Public Adjuster

For straightforward, relatively contained water damage claims, a burst pipe affecting one room, a clear and quickly-resolved cause, a cooperative insurance company, most homeowners can work directly with their insurance company’s adjuster without needing additional representation. A good restoration company’s documentation is often sufficient to support a claim of this size moving smoothly.

When a Public Adjuster Is Worth Considering

- Your claim is being disputed or significantly undervalued compared to what the actual repair costs are turning out to be

- The damage is extensive, affecting multiple rooms, structural elements, or requiring temporary relocation

- You’re unsure what your policy actually covers and want someone who reviews policies professionally to identify coverage you might be missing

- Your insurance company is slow to respond or seems to be delaying the process without clear explanation

- You’ve already received a settlement offer that seems low relative to actual repair estimates from contractors

Public adjusters typically charge a percentage of the final settlement (commonly in the range of 10-20%, though this varies and should always be confirmed and put in writing before hiring one), so it’s worth weighing this cost against how much a more favorable settlement might realistically add, particularly for larger claims where the percentage fee is more likely to be worthwhile relative to a meaningfully improved outcome.

Can You Use Both at the Same Time?

Yes, and for larger or more complicated losses, this is actually a common and effective combination. The restoration company handles the physical work and provides detailed technical documentation (moisture readings, photos, scope of work, material costs), while the public adjuster uses that documentation, combined with their own assessment, to negotiate the claim with your insurance company. The two roles complement each other rather than overlapping: the restoration company focuses on actually fixing your property, the public adjuster focuses on the financial and negotiation side of the claim.

What to Look for in a Public Adjuster

- Active license with the California Department of Insurance

- Clear, written fee structure before any work begins

- Experience specifically with water damage or flood-related claims, not just general property claims

- Willingness to provide references from past clients

- Transparent communication about realistic outcomes, rather than promising a specific dollar amount before reviewing your policy and damage in detail

What to Look for in a Restoration Company (If You Haven’t Hired One Yet)

If you’re navigating this process and haven’t yet hired a restoration company, that decision typically comes first, since you need the physical damage addressed and documented before a claim can move forward in any meaningful way. See our guide on how to choose a water damage restoration company for what to check before hiring one.

How Public Adjuster Fees Actually Work in California

California regulates public adjuster fees and licensing through the Department of Insurance, and fee structures are required to be disclosed in writing before any work begins. While percentage-based fees are standard, the exact percentage is negotiable and can vary based on claim complexity and size, larger, more straightforward claims sometimes command a lower percentage than smaller, more contested ones, since the adjuster’s time investment doesn’t scale perfectly with claim size. It’s reasonable, and expected, to ask multiple public adjusters for their fee structure before choosing one, the same way you’d compare quotes for any other professional service.

Red Flags When Evaluating a Public Adjuster

- Unsolicited contact immediately after a disaster. Be cautious of public adjusters (or anyone claiming to be one) who show up uninvited at your property immediately after a fire, flood, or storm, sometimes called “storm chasers.” Legitimate adjusters generally don’t need to solicit business this aggressively.

- Pressure to sign a contract immediately, especially one with an unusually long commitment period or one that’s difficult to cancel.

- Guaranteed settlement amounts before any actual review of your policy or damage. No legitimate adjuster can honestly guarantee a specific dollar figure upfront.

- Reluctance to provide their license number or any pushback when you mention verifying it with the California Department of Insurance.

What Happens If You and Your Insurance Company Still Disagree After Using a Public Adjuster

If negotiations through a public adjuster still don’t resolve a disputed claim, most policies include an appraisal process as a next step, a formal procedure where each side selects an independent appraiser, and those two appraisers select a neutral umpire if they can’t agree. This process is generally faster and less expensive than litigation, though it’s typically reserved for disputes over the amount of a covered loss, not disputes over whether something is covered at all. For coverage disputes specifically (rather than valuation disputes), legal counsel specializing in insurance claims may become necessary, though this is generally a last resort after other avenues have been exhausted.

How a Public Adjuster’s Documentation Differs From a Restoration Company’s

It’s worth understanding that these two forms of documentation, while related, serve different purposes and aren’t interchangeable. A restoration company’s documentation is primarily technical: moisture readings, photos of physical damage, a detailed scope of work and materials needed to repair the property to its prior condition. A public adjuster’s documentation is primarily valuation-focused: a comprehensive inventory of everything affected (including depreciation calculations, replacement cost estimates, and sometimes additional living expenses if the property is temporarily uninhabitable), framed specifically in the language and structure an insurance company’s claims process expects. A public adjuster will typically request and review the restoration company’s technical documentation as a foundation, then build a more complete valuation package on top of it, rather than starting from scratch.

What Happens When the Restoration Company and Public Adjuster Disagree on Scope

Occasionally, tension can arise if a public adjuster believes the restoration company’s scope of work is either understated (missing covered damage) or overstated (including work the adjuster feels exceeds what’s necessary to restore the property to its prior condition). In these situations, it’s worth having a direct conversation between all three parties (you, the restoration company, and the public adjuster) rather than letting the disagreement play out indirectly through separate conversations. A reputable restoration company should be able to clearly justify their scope based on actual moisture readings, material assessments, and industry-standard repair practices, which generally resolves most of these disagreements without much friction.

How to Verify a Public Adjuster’s License Before Hiring

Before signing anything, you can directly verify a public adjuster’s license status through the California Department of Insurance’s online license lookup tool, which shows whether the license is active, any disciplinary history, and the specific lines of authority the adjuster is licensed for. This takes only a few minutes and is worth doing even if the adjuster was personally referred to you by someone you trust, since license status can change and referrals don’t always reflect current standing. It’s also worth asking how long the adjuster has been licensed specifically in public adjusting (as opposed to having worked previously as an insurance company adjuster before transitioning), since the two roles, while related, require different skills, particularly around negotiation from the policyholder’s side rather than the insurer’s side.

What Happens to the Public Adjuster Relationship Once the Claim Settles

Once a claim is settled and the public adjuster’s fee is paid from the settlement proceeds, the relationship typically ends, since public adjusters are engaged for a specific claim rather than an ongoing advisory role. If a new, unrelated issue arises with the same property later, even from a similar cause, a new engagement (and potentially a new fee arrangement) would generally apply, since the original contract was scoped to the specific claim being resolved. This is worth keeping in mind so you don’t assume an existing public adjuster relationship automatically extends to future, separate incidents.

A Realistic Timeline of How These Two Roles Interact

In a larger claim, the sequence often looks like this: the restoration company is called first for emergency mitigation, since stopping ongoing damage takes priority over any insurance paperwork. While mitigation is underway, the homeowner files the initial claim with their insurance company. If the homeowner decides a public adjuster makes sense, often after receiving an initial settlement offer that seems low, the public adjuster is brought in to review the policy, the restoration company’s documentation, and the insurer’s offer, then negotiates from there. The restoration company typically continues independently with the actual repair work throughout this negotiation process, since the physical recovery of the property generally shouldn’t be delayed waiting on a settlement to be finalized.

Quick Reference

| Restoration Company | Public Adjuster |

|---|---|

| Physically repairs the property | Negotiates the insurance settlement |

| Documents damage as part of the repair process | Reviews policy and values the full extent of loss |

| Paid for the actual restoration work | Paid a percentage of the final settlement |

| Needed for nearly every water damage event | Most useful for larger, disputed, or undervalued claims |

For more on how the claims process generally works in Los Angeles, including what’s typically covered, see our complete guide on water damage insurance claims.

Dealing with water damage and not sure where to start? Call ASAP Water Damage Restoration. We handle the physical recovery and provide the thorough documentation you’ll need, whether you work directly with your insurer or bring in a public adjuster.